Of Dead Historians and Geopolitics

The year 430 BC turned out to be a pivotal year for the Greek city states of Athens and Sparta. During the second year of the Peloponnesian War, a plague epidemic broke out in the dominant city state of that era, Athens. The “Plague of Athens” as it is known, killed an estimated 100,000 people in the region of Attica over a period of two years. Historians estimate that the region had a population of 300,000 so the epidemic killed a massive 1/3 of its inhabitants.

The historian Thucydides (460-400BC) describes in some detail how the plague originated in Africa, the wide and fast spread in Athens, the suffering of the patients and the struggle of doctors to contain it while putting themselves in harm’s way with many falling ill in the process. Sounds familiar ?

“Words indeed fail one when one tries to give a general picture of this disease; and as for the sufferings of individuals, they seemed almost beyond the capacity of human nature to endure. The most terrible thing was the despair into which people fell when they realised that they had caught the plague; for they would immediately adopt an attitude of utter hopelessness, and by giving in in this way, would lose their powers of resistance. As for offences against human law, no one expected to live long enough to be brought to trial and punished: instead everyone felt that a far heavier sentence had been passed on him.”

-Thucydides

The Athenians were engaged at that point in time in a savage war with the Spartans. And although the war kept on going for two more decades, the plague determined not only the outcome of the war but also the path of Greek and world history. Pericles, the leader of democratic Athens perished in the epidemic along with a lot of significant statesmen. At the end of the war a pro-Sparta oligarchy of tyrants ruled Athens and its people. That was the first blow to Demarchy, the ancient Greek method of democracy that is not really mentioned or taught extensively nowadays as it is democracy possibly at its best, without the burden of self serving elites that our current “democracy” suffers; but that is another long story.

One can make their own parallels to the current situation but before looking at what this could teach us, let’s move to the present. Harvard professor Graham Allison coined the term “Thycydides Trap” to describe the situation where the rivalry between an established power and a rising one often ends in war. In the same way Athens’ meteoric rise to power (via trade, technology, science and the arts) triggered a reaction by the dominant military power of Sparta, the current setup of a dominant United States vs a rising China may trigger the same clash. In fact history suggests war has inevitably been the outcome of these tensions between dominant powers and challengers. Many doubt WWIII is a viable path in an era of mutually assured destruction nuclear weapons. But is war the only possibility ?

“Knowing where the trap is—that's the first step in evading it.”

― Frank Herbert, Dune

Before the pandemic, the trade tensions between US and China were at the center of attention and the drivers of market volatility. Post pandemic they may or may not return to the foreground. The realities of the post-covid world are becoming clearer every day. In particular globalisation has stalled and is probably in reverse. The Chinese focused global supply chain will slowly but surely change. Global travel will not recover soon. Demand patterns will fundamentally change. Less “stuff” will be moved around the world and used. Tariffs will have gradually less of an impact. Digital business will thrive.

So putting together the plague of Athens and the Thucydides trap narrative where can one see things going ? Given 21st century technology I would say the current pandemic is not in itself enough to topple the US as the dominant global player, at least not immediately. However, the effects of the plague were felt decades after its end in ancient Greece and there are hints the same long term thematics may be at play.

A reduction of democracy, centralisation of power driven by monetary policy (the big enterprises benefiting disproportionally), a widening gap between rich and poor and dominance of technology platforms. At the same time China is already there. There is no hint of democracy, the party holds absolute power over public and private enterprise. The elites function differently in the US and China but the effect is the same. The pandemic will only accelerate the transition of the US into a power that is closer to China in some ways than its former self surprisingly.

What about Europe in all this ? In my view, the EU is quickly moving to the role of an irrelevant coalition of trading partners, inwards looking and bureaucratic; a coalition of the weak. A strong coalition (or even better a federation) with common economic and foreign policy, might have been able to emerge out of this as the new global leader. This is not the case; cultural and historical reasons sadly explain why.

“War is a matter not so much of arms as of money.”

― Thucydides, History of the Peloponnesian War

In the end a “war” will happen. But this time it will be an all out war around the global reserve currency and spheres of economic influence rather than guns. Debt capacity vs inflation and monetary trust will be a central theme. Technology will play a central role in this conflict, only this time in controlling the flow of information with AI devouring jobs at an increasing rate while creating all powerful data monopolies. The reversal of physical globalisation may hurt China mortally or force it to grow and evolve in other unexpected ways. It remains to be seen who comes on top in this “war” as the situation develops over the next decade.

The pandemic just pressed the fast forward button on all this and the choices we all make now will determine much more than next quarter’s GDP. The outcome will not only shape the lives of billions of people but also the future of our planet.

“Those who fail to learn from history are condemned to repeat it.”

-Winston Churchill

Some tweets from this past week

Markets

Let me take a step back after two months of weekly newsletters to asses the situation. The market has been flooded in liquidity. In the process, both equities and bonds are now untethered from any kind of economic reality. The type of value opportunities I was hoping to explore within say a 6-12 month timeframe disappeared in an ocean of printed money in a matter of days.

I would have preferred a different short term outcome, where active strategies in more asset classes would have shined. For the curious and independently minded investors I still advocate to look into those; I am available to discuss with interested readers.

I believe there will be a new and harsh reality check around the end of the summer. August to October has been historically a time of financial market stress. After the written-off Q2 results are out, the handouts spent and the pandemic cheques used up, there may be another bout of reality triggered volatility. Maybe that also gets solved by another few trillion dollars or so; maybe not. I have decided I will refrain from publishing trading strategy ideas here, at least not in the same open format. If there is enough interest, I will resume posts with markets strategy ideas in some form, probably for a closed group of interested and engaged participants. In the meantime, I will continue to write shorter occasional newsletters with mostly a markets thematic.

Transparency Time

As a trader I found in the last two months some compelling opportunities that I posted in the newsletters and other channels and in the spirit of transparency I will make a quick recap. This is not to prove that there were valuable nuggets of advice in these posts (there were !) but mainly to demonstrate money can be made in all types of market regimes and not just by passive equity long beta. I am also a numbers guy; P/L never lies. Macro stories are nice and make good blog post material but the investing bottom line is about committing capital and the associated profits and losses. Skin in the game and performance is the part of the equation that often gets lost in follower counts.

So here goes for the record:

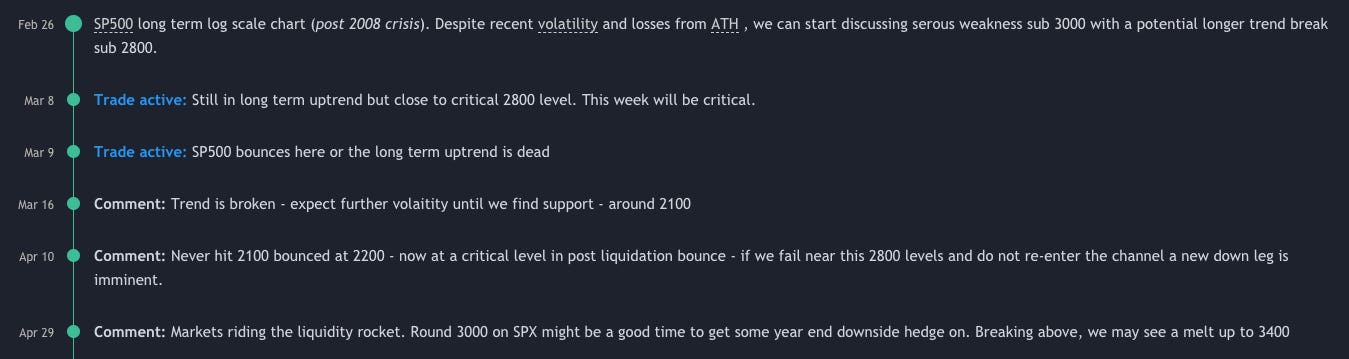

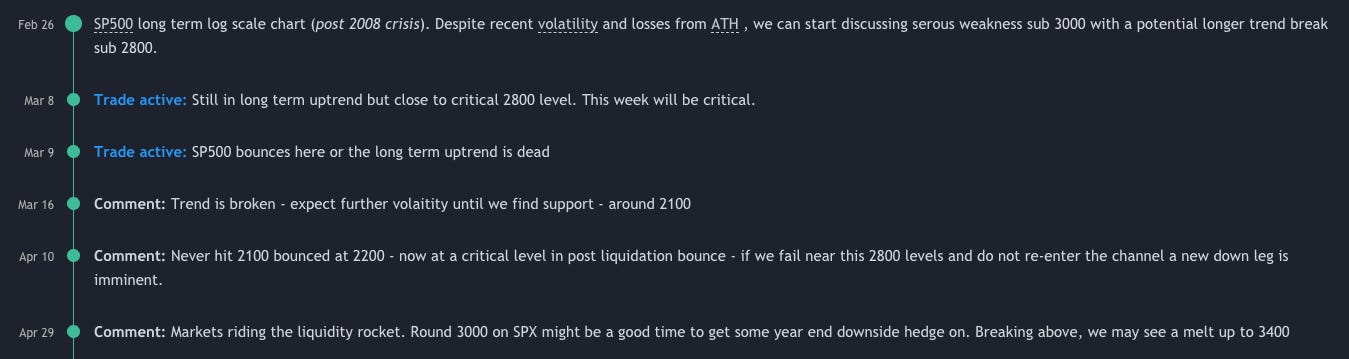

SP500 Mea Culpa : I did not believe the equities rally. I did not short it (thankfully !) but I had nevertheless a big opportunity loss on a decent move up. I am thinking we may see a melt up in the region 3100-3400 till a new reality check. In my defence I thought levels around 2000 were entries but did not expect the rebound would happen from higher levels and so fast. PL = 0.

Short Equities vs Long Gold : SPY/GLD PL = +6.66%

Short volatility VIX @ 80 : PL = 40+ vol points in the money - call it +50% but it depends a lot on how this was executed (futures, options, …). This one was my favorite trade for so many reasons …

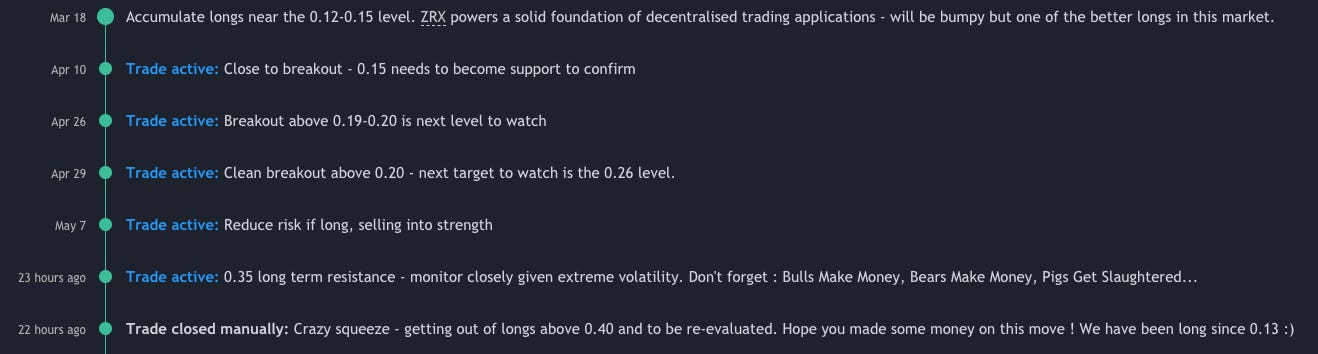

Crypto : ZRX token long PL = +223%

Commodities : CRB PL = +4.9% (chart here)

Airlines : Lufthansa cheeky long PL = +1.3% (chart here)

Refiners Crude recovery trade : CRAK vs SPY PL = 0 (chart here)

Balanced Defensive Portfolio (suggested 5th April) : PL = +28.2%

Metals: Silver long PL = +0.6%

ETF Value play : DVP PL = 0

ETF Value Play : VLUE PL = +3%

ETF Value Play : IWN PL = +5.4%

Energy majors : XOM PL = +9.65%

Energy majors : RDS-B = -4.49%

Energy index options : XLE Sep40 & Sep45 Calls PL = 86%

So net-net this quick transparency exercise shows :

15 bets (14 really as I never stepped into the SP500 index trade either way) : 11 positive, 3 flat, 1 negative.

Best trade up +223%, worst trade down -4.49%.

Average Return : 27.6% over 2 months

I have not included positive p/l on my longer term outright positions in Gold & Crypto or my systematic models; only the trading sample of the last 2 months that I have posted real time in public is here.

I will take that as a good open experiment with major indices flat(ish) on the year including a major drawdown/death dive towards the abyss.

Onwards and upwards !

“There is only one side of the market and it is not the bull side or the bear side, but the right side.”

- Jesse Livermore

I sometimes post markets commentary on Twitter and positioning ideas on TradingView and on Telegram. Feel free to connect with me on LinkedIn.

If you find this newsletter useful or interesting, and want to show your appreciation, the best way to do that would be to sign up, share it on your social media, or forward it to someone you think might get some value out of it.